How Government Policy Dismantled Manufacturing in Australia and Canada

Explore how deliberate government policies led to the decline of manufacturing in Australia and Canada, reshaping their industrial landscapes over decades.

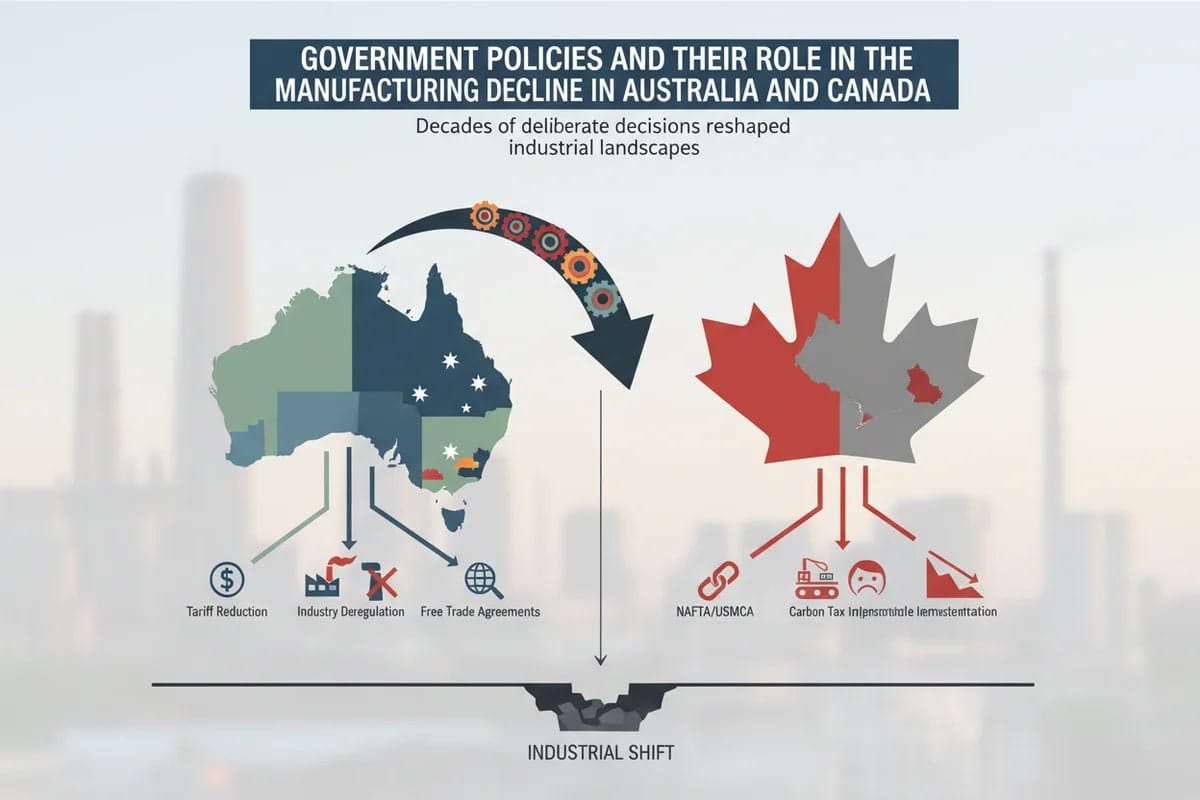

Manufacturing decline rarely happens by accident. In both Australia and Canada, the erosion of industrial capacity over the past four decades reflects a series of deliberate and passive policy choices that, taken together, redirected capital away from domestic production and toward consumption, services, and offshore supply chains. For COOs building industrial businesses and investors allocating capital to manufacturing ventures in either country, understanding the policy architecture that produced this decline is not merely historical interest — it is essential context for assessing where structural risk still sits and where genuine opportunity is beginning to emerge.

The Scale of What Was Lost

Australia's manufacturing sector contributed roughly 30% of GDP in the 1960s. By the early 2020s that figure had fallen to approximately 6%, placing Australia among the most deindustrialised wealthy nations on earth. Canada followed a similar trajectory, with manufacturing's share of GDP declining from around 20% in the 1980s to approximately 10% by the mid-2020s, according to data reviewed in the OECD's assessment of Canadian industrial policy. In absolute dollar terms, Statistics Canada data shows that manufacturing output sat at roughly CAD 200 billion annually in recent years, a figure that masks the deeper problem of productivity stagnation and the near-total absence of scale-up among innovative manufacturing firms. Australia's manufacturing output, measured in current prices, has hovered around AUD 100 to 110 billion per year in recent reporting periods, a number that looks stable on the surface but conceals the collapse of value-added complexity in what is actually being produced domestically.

These are not simply the natural consequences of comparative advantage or globalisation. They are the downstream effects of specific policy decisions made in Canberra and Ottawa over decades.

The Policy Choices That Accelerated Decline

In Australia, the most consequential shift came through the progressive removal of tariff protections between the 1980s and the 2000s, a process that was philosophically sound in its intent but was not accompanied by any serious transition support for the firms and workforces it displaced. The automotive industry is the clearest example. Rather than using the transition period to build alternative manufacturing capability in adjacent sectors such as advanced materials, precision engineering, or defence supply chains, successive Australian governments allowed the industrial base to hollow out without replacement. Tax policy compounded the problem. The research and development tax incentive, while nominally supportive of innovation, was structured in ways that benefited software and services businesses far more readily than capital-intensive manufacturers, who face longer development cycles, higher upfront expenditure, and more complex eligibility assessments.

Canada's policy failures operated through a different but equally damaging mechanism. The OECD's review of Canadian industrial policy identified slow productivity growth and weak business investment as structural problems that policy had failed to address, and in some cases had reinforced. Canada's tax treatment of manufacturing investment has historically been less generous than that of the United States, creating a persistent incentive for Canadian manufacturers to either offshore production or to simply not scale. The proximity to the American market, which might logically have encouraged Canadian manufacturers to build export-oriented capacity, instead created a dependency where Canadian firms often served as branch operations or suppliers to American multinationals rather than developing independent industrial capability. Federal support for small and medium-sized enterprises existed in various forms, but the OECD assessment noted that the effectiveness of these programs varied considerably, with limited evidence that they were successfully converting innovative SMEs into scaled manufacturers.

Both countries also shared a common failure in the treatment of critical industrial infrastructure. Neither government made sustained, long-term commitments to the energy pricing, logistics networks, and skills training systems that manufacturing-intensive economies like Germany, South Korea, and Japan maintained as foundational policy priorities. Without competitive and reliable industrial energy costs, without deep vocational training pipelines, and without procurement policies that systematically favoured domestic manufacturers, the underlying conditions for industrial investment remained structurally weak regardless of whatever incentive programs sat on top.

Recent Attempts at Reversal

Australia's most significant recent policy response is the Future Made in Australia Act 2025, backed by a AUD 22.7 billion investment commitment over a decade. The centrepiece of the production incentive framework is the Critical Minerals Production Tax Incentive, which offers a 10% tax offset on eligible processing expenditure for critical minerals processed between 1 July 2027 and 30 June 2040. A parallel incentive covers green hydrogen production. The IEA has catalogued this act as a substantive industrial policy intervention, and in the context of Australia's recent history it represents a meaningful departure from the passive approach that characterised the previous three decades.

The logic is defensible. Australia holds some of the world's largest reserves of lithium, cobalt, nickel, and rare earth elements, and the global energy transition creates genuine demand for processed critical minerals that Australia is currently exporting in raw form at a fraction of the value it could capture through domestic processing. The 10% tax offset is not transformative on its own, but it is a signal of policy intent that, combined with the broader AUD 22.7 billion commitment, creates a more credible investment environment for capital-intensive processing facilities than has existed in Australia for a generation.

Canada's recent industrial policy has similarly oriented toward clean technology and critical minerals, with federal programs targeting SME support and technology development. However, the OECD's assessment, which examined Canada's industrial policy framework as of 2026, identified persistent structural challenges that short-term incentive programs are unlikely to resolve. The core problem in Canada is not the absence of innovative firms but the failure to scale them. Canadian companies that develop manufacturing technology or industrial processes frequently commercialise in the United States or are acquired by foreign firms before they reach the scale at which they would generate significant domestic industrial employment and output.

What the Numbers Actually Tell Investors

For an investor or COO evaluating manufacturing opportunities in either country, the comparative picture reveals both the depth of the problem and the nature of the opportunity. Australia's AUD 100 billion manufacturing base is heavily concentrated in food processing, metal products, and construction materials, with limited representation in the high-value advanced manufacturing categories that generate the most durable industrial employment and export earnings. Canada's CAD 200 billion base is larger in absolute terms and more diversified, with meaningful aerospace, automotive components, and pharmaceutical manufacturing, but the productivity gap relative to American peers remains a persistent drag on competitiveness.

The policy incentives now coming online in Australia are targeted specifically at the sectors where Australia has genuine resource advantages, which is a more strategically coherent approach than the generalised support programs that characterised earlier decades. The 10% critical minerals processing offset, applied over a thirteen-year window from 2027 to 2040, provides enough duration for investors to underwrite capital-intensive processing infrastructure with some confidence in the policy environment. That said, critics of both the Australian and Canadian approaches are correct to note that tax incentives alone do not resolve infrastructure deficits, workforce skills gaps, or the cost disadvantages that Australian and Canadian manufacturers face relative to producers in Southeast Asia and China. A processing facility that benefits from a 10% tax offset but faces energy costs three times higher than a competitor in Malaysia is not automatically viable.

The Structural Argument That Policy Has Not Yet Addressed

The most sophisticated critique of both countries' industrial policy trajectories is not that they have done too little recently but that the decades of neglect created structural conditions that are genuinely difficult to reverse through fiscal incentives alone. When a country loses manufacturing capacity, it also loses the supplier ecosystems, the engineering talent pipelines, the institutional knowledge embedded in firms, and the cultural familiarity with industrial problem-solving that makes manufacturing investment viable. These are not things that a tax offset restores. They require sustained, patient capital commitment from both government and private investors over periods measured in decades rather than budget cycles.

For founders building manufacturing businesses in Australia or Canada today, the policy environment is meaningfully better than it was ten years ago, but the structural inheritance of deindustrialisation means that building a manufacturing business in either country still requires solving problems that would not exist in economies that maintained their industrial base. Supply chains are thinner, skilled trades are scarcer, and the institutional knowledge that experienced manufacturing workforces carry has partially dispersed. These are real costs that do not appear in a tax incentive calculation but absolutely appear in a project budget.

What Comes Next

The honest conclusion for investors and operators is that both Australia and Canada are in the early stages of a genuine industrial policy reversal, but the gap between policy intent and industrial reality remains large. Australia's AUD 22.7 billion commitment and Canada's various clean technology and SME programs represent a change in direction rather than a restoration of capacity. The opportunity for founders and investors lies precisely in that gap, in building the processing facilities, component manufacturers, and industrial technology businesses that policy is now designed to support but that the market has not yet supplied at scale. The risk lies in overestimating how quickly policy signals translate into the deep industrial ecosystems that make manufacturing businesses genuinely competitive.